The 600 Group plc (SIXH)

Laser focused?

TL;DR Old industrial business selling well below book value. Recently downsized with focus on high-growth, higher margin segment. Upside if new focus works, limited downside.

I’ve recently read everything I could find about Walter Schloss an alumnus of Benjamin Graham and a superinvestor featuring in Buffett’s famous article. He had a fairly simple formula for investing → Buy stocks cheap. Best source of info on him is here - https://www.walterschloss.com/

He originally used the Ben Graham formula of buying stocks below net working capital (NWC) value. Meaning take NWC = (Current Assets - Current Liabilities - Long Term Debt) and if it’s say 30% more than market cap then buy. Buy a lot of these companies and in aggregate you’ll make money. He had a portfolio of about 100 stocks and sold them pretty mechanically after they made about 50% profit. He also made a point that you only know a stock once you own it. In that spirit when he identified a stock purely on statistical measures, he would buy it and then only send for the annual reports - well these were the pre-internet days mostly.

That used to work but then in the 60s these stocks largely disappeared. They do reappear from time to time but not often. When it stopped working he changed his approach to buy stocks below or at book value. He preferred companies with little debt and in temporary problems. Usually these were secondary industrial stocks.

I’ve created a simple screen for below book value companies. It produced some 400 companies in the UK alone. In my results I have the description of the company as well. I’m going through them and looking for businesses I can sort of understand. I’ve excluded all the miner/explorers.

When I find something interesting I look at their financials to see earnings and historical earnings. I found a few interesting ones but dismissed them after reading their annual reports.

Then I stumbled upon The 600 Group Plc. Never heard of it before. It’s a very small cap company but with a rich history. They have been around for about 100 years. They were in all sorts of engineering businesses over time but in the last 30 or so years they mainly shifted to owning industrial laser businesses. They have very recently disposed of their Machine Tool Solutions division which makes them a pure laser player with higher margins and growth potential then before.

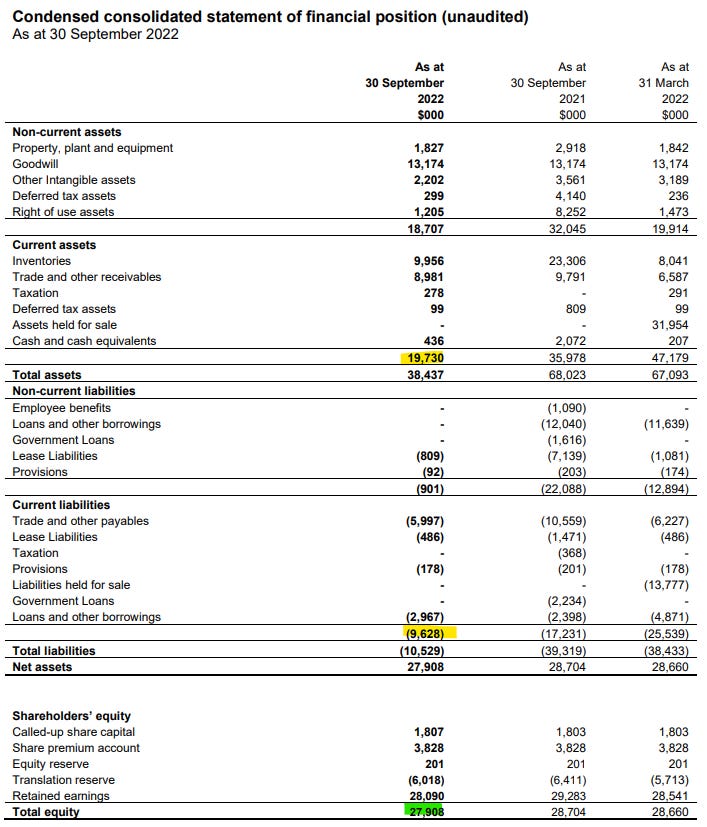

Looking at the balance sheet from the interim results as of 30 Sept 2022:

Walter would be pleased - net working capital of around $10m (yellow above → Current Assets - Current Liabilities - Long term debt). Their market cap is around £11m. At the moment the pound buys about 1.22 dollars so market cap is about $13.5m. Not quite margin of safety in terms of NWC the old Graham way but it’s almost there.

Book value (green) still about twice the market cap. That’d be quite good by Walter’s standards.

Do they make money? Yes and historically they were fairly profitable. They lost their way a bit due to Covid as did a lot of other companies. These are the numbers for Profit before tax in $ millions (adjusted):

The above numbers are mostly for when they still had the machine tooling division. Year 2022 is without it. I checked earlier segmental numbers and I think they could conceivably keep on making $1m PBT - hopefully more with just the lasers.

If that was the case that would put them in EBIT/EV ~ 1/13 ~ 7.5% which is obviously not so great. However, the laser segment was the one growing and it grew again this year in terms of sales by 12% (on previous half year results).

Now, one aspect of the business I’m not so keen on is that the management pay themselves quite a bit - about $900k in total in 2022. In fact if you could buy the whole enterprise your owners earnings (since you could probably reduce the management cost) would be almost $2m meaning the EBIT/EV would suddenly be 15%. Still not awesome but better.

That is somewhat offset by the fact that the exec chairman owns 20% of the company via an investment vehicle. It should be in his interest to treat shareholders well.

Return on Capital?

Not so great if we consider the potential PBT of $1m and capital employed as (Total Assets - Current Liabilities) = $28m - it’s about 3.5%. If we exclude Goodwill on the premise that what’s done is done - we’d get about double that so 7%. These are bad figures for sure. Can they increase profits without also having to increate their capital massively? We’ll see.

Forward visibility - they have order book for about quarter of their revenue as of September 2022.

Some more assets?

From annual report 2022:

The UK holding company continues to benefit from previous tax losses with $1.6m of deferred tax asset not recorded on the balance sheet. No taxation is payable in the UK. There are substantial deferred tax assets in the USA of $2.5m that are not recorded on the balance sheet. The US businesses are subject to Federal taxation on their profits at the rate of 21% but also suffer State taxes which increases their overall composite rate to 25%.

Not sure why this is not balance sheet. Anyone?

No long-term debt

From annual report 2022:

Net bank indebtedness of $6.3m at 31 March 2022 (2021: $4.8m) was all cleared in April 2022 following the receipt of the proceeds on the Machine Tool Division sale. The USA working capital credit line was increased to $10m to facilitate additional requirements to support the substantial order increases during the year and was reduced in April 2022 to $7.5m following the sale of Machine tools.

As of September 2022 they have about $3m short term debt.

Industry

Industry predictions for the laser industry expect the volumes to continue to increase at high single digit percentage levels going forward.

However their share of the industry is tiny so they can grow aggressively in this segment. Especially in the US - there is potential for reshoring of production to US.

Catalyst

From 2022 annual report:

Fiscal 2022 was a truly transformative year for The 600 Group PLC. After more than 100 years of owning and operating various, often unrelated, businesses in a number of industries in various countries around the world, the group has simplified itself and is now engaged in only one line of business with current manufacturing and executive facilities in only one country, the United States. The group has transitioned from being a leveraged manufacturer of legacy products in mature industries to a business that was debt free at the date of the machine tool disposal and is now focused, flexible and embracing 21st century technology with inherent attractive growth rates and ample opportunities, both internal and external, to expand its existing capabilities.

The sale of our machine tool business, concluded in April, allowed us to redeem all long-term debt while we remain with significant credit facilities. This enables us to support the increased level of activity in our remaining division, Industrial Lasers, where revenues increased by 50% and year-end order book has grown by 24%.

I think the above change is not taken into account by Mr Market. Looking just 10 years back into their annual report this was a sprawling conglomerate with operations in South Africa, Australia etc. Now it’s a streamlined small business with focus on industrial lasers. If this comes to pass we should see multi-year 20% pa revenue growth, 10-12% operating profit margins.

Nobody is following them at the moment.

Further they have mandate to repurchase about 10% of their shares.

Comparables

They are too small to be compared with anything but in lasers Coherent has similar ~ 10% operating profit margin, much higher multiples.

Risks

If they don’t control their expenses - there have been some signs of that - in the last six months their expenses grew by two million in spite of them operating as a smaller business. They blame it on post-covid supply issues + inflation. We’ll see…

The main risk I see is they buy some add-on laser focused business at a stupid price financed by debt.

They just removed their CFO - good sign? I doubt it but I'm holding on...

excellent write up!